I wanted to do a review of a property outside of the normal area I look at for rentals, so for this post I have decided to look at potential rentals in Union County, NC. As usual, I am focusing my analysis for rentals on North Carolina, as the property taxes do not change between a primary residence or a rental property. Buy and hold rental investing is definitely possible in South Carolina, you just have to look at each deal individually and see how the numbers work for you.

For this 30 year return analysis, I am looking at a property in Waxhaw. The property is located in the Cureton Community and is currently listed for $300,000. Click here to view the listing (if it is still active).

I chose this property because it is less than 10 years old, so should have plenty of life left to it before any major repairs are needed, and a similar floor plan rented recently for $2,095 a month, and this is the basis we will compare this property to.

The Annual Property taxes for this home are $3,120 and annual HOA is $550. I have estimated insurance for this home at $1,200 per year. By putting 20% down with a 5% interest rate on the property, your total payment of Principal, Interest, Tax, and Insurance (PITI) plus HOA comes to $1,694 per month.

With an expected rent around $2,095 per month, this represents $400 of positive cash flow! Not bad for a property that took about 15 minutes to choose, but we need to be a little cautious here. Most investors will want to consider vacancy costs, maintenance costs, and property management. Since this property is fairly new and vacancy in the area is very low, I am going to allot 4% of the monthly rent to each of these items. Property management costs can vary, but I will allocate 10% of the rent to this. By factoring in these items, our monthly income is down to $1,717. Still slightly cash flow positive.

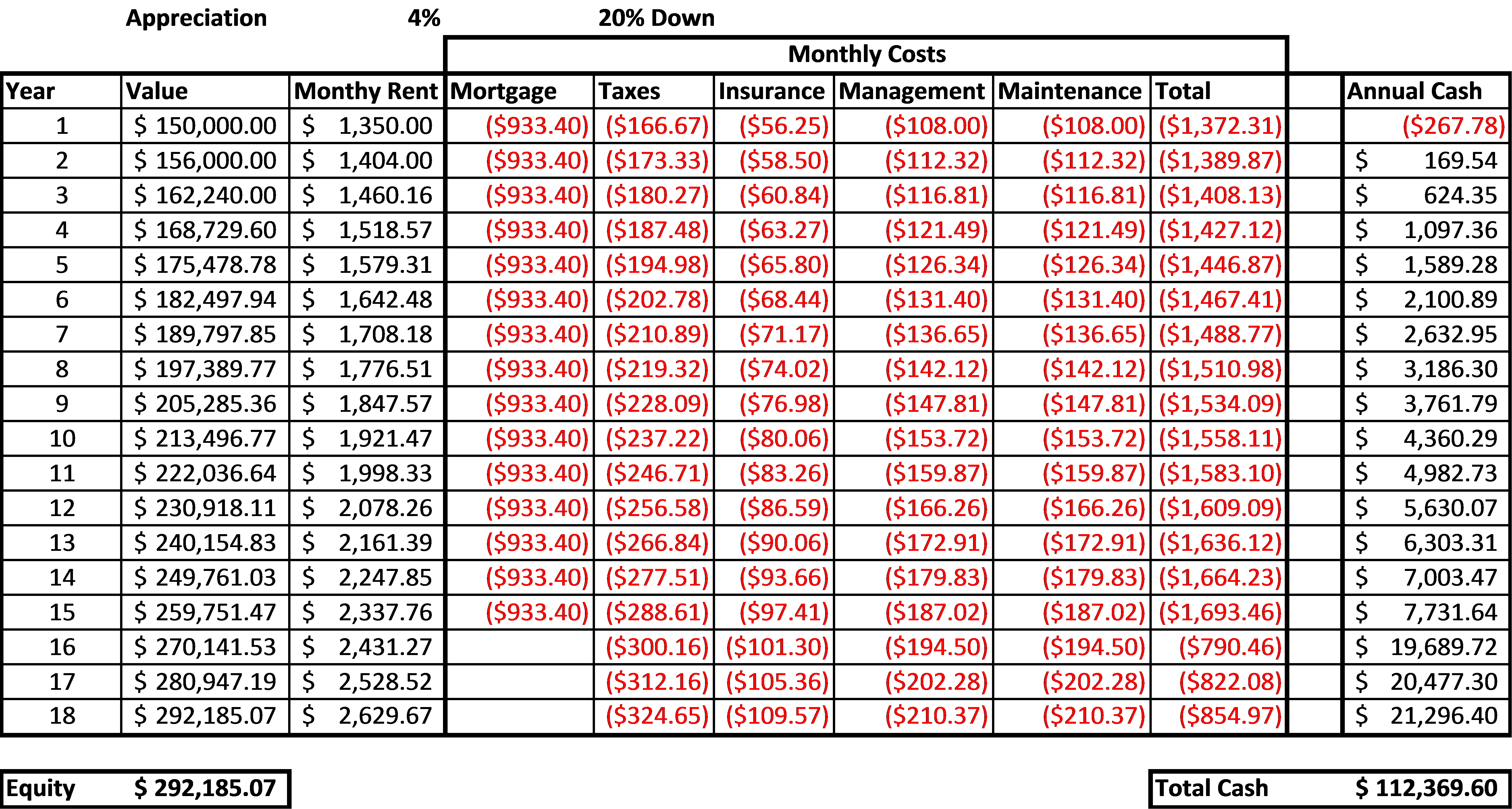

What we need to look at are the future returns of the property, the future value, and overall 30 year return. Since we have used a 30 year mortgage, the home will be owned free and clear at the end of the period, and all other expenses are rolled in so the only investment would be the initial down payment on the home.

One of the great things about this situation is that over the 30 years, the rents will increase while the mortgage payments remain fixed. Taxes and insurance will also increase, and I will calculate those increases relative to the value of the home. Standard rent increases are 3-5% annually, so I will use a 4% increase, and a home appreciation rate of 3% annually.

To put things into perspective, this results in the home being valued at just over $700,000 when it is paid off, with annual expenses of about $40,000 and monthly rent of about $6,500. Over the course of the 30 years of owning the home, a cumulative profit (rental income after expenses plus home equity) of $1,112,310 will be achieved, and using $65,000 as your initial investment ($60,000 down plus closing costs), this represents an annualized rate of return of 9.93%.

Another way to look at this, perhaps you were to purchase a home when your child was born as a college savings plan. After 18 years in this scenario, the cumulative profit would be around $430,000. Who knows what college will cost 18 years from now, but that is a solid foundation to paying for any education!

This analysis is for informational purposes only and is not guaranteed, but if you have any questions about how I came up with these numbers or about how we can make something like this work for you, please don't hesitate to contact me!